Open and closed models are on different exponentials

Interconnects by Nathan Lambert · Monday, June 1 2026 · 7 min read · ↑ top

Where marginally higher intelligence drives value, and where it doesn't.

Listen to post · 7:21

The largest debate that’ll define the future balance of power between the open and closed AI model ecosystems is primarily economic — it’s if users of AI will continue to pay dramatically more, i.e. large margins, for the top closed models. Early 2026 is a seminal time for the AI industry, as the coding agents¹ have shown the first area where a huge AI market will continue to pay a substantial premium for better intelligence.

The other side of this dichotomy is the inevitable decay of API businesses at these same labs. These labs will realize they need to protect their best models, rolling them out later in APIs to both protect token supply, avoid distillation, and stick to use-cases with higher margins. All of these effects will be clearly visible in 5-10 year timelines, as in the near term markets, prices, margins, and demand will be dictated by a rapid buildout of compute (supply-limited in the near term) and mass subsidization of tokens (through continued investment in new AI companies).

The core of this argument rests in the obvious habit changes that are setting in with coding agents past the Opus 4.5 and Codex 5.2 thresholds. People are not making this switch because they are lazy, but because their net output is obviously higher when using an agent as an implementation aid for complex knowledge work. For people who rely on coding agents to work, they will always pay more for the best rather than settle for good enough. There are so many ways to make the product better, speed, intelligence, specialized models, etc.

I would pay $2000/month for the tools today, especially knowing they’ll get much better. At the same time, it is likely that many companies are forcing agents and usage onto people that actually will get very little out of them in their current form, which helps the AI buildout (or bubble) continue.

The best closed labs — right now this list is just Anthropic and OpenAI, but it’s reasonable to expect Google to catch up — will always make the most efficient models for intelligence at a given cost. Building models is a mass capital investment of talent, data, and compute. These systems, a combination of model weights, harnesses, tools, and serving infrastructure have massive returns on integration (where open models are designed to work across many, diverse serving situations). These integration benefits — the integration of hardware and new forms of software — can be expressed in any possible way of making models better.

The models in the near future may saturate on benchmark scores, but if that intelligence ceiling really is a cap on utility then the labs will optimize utility per second or per watt, serving users in another way. Improving the models is possible in every direction — there have been no walls in progress. We’re early in the mass buildout of intelligence, which involves harnessing the physical world to build numerous datacenters, organizing many AI researchers so that a large team can contribute to one model, and of course solving many small, low-level puzzles that unlock performance. Every indication is that there is still meaningful performance to be unlocked and the closed labs are the best set up to extract it.

The collective wisdom of the labs is that making the models smarter, in terms of the frontier of absolute intelligence, has the most value. This is the right call to me because it unlocks large new markets. Optimizing models at a fixed intelligence level locks in markets, expands accessibility over time, and increases return on investment for users (while potentially lowering margins for selling intelligence).

Many people are making this bet that models will keep getting better and are learning to work well in these harnesses, even though some workflows are still a bit clunky. This is the right bet. These people all will continue to use the absolutely best models available. It’s like buying an iPhone as a consumer. You could get an Android and suffer from a bunch of paper cuts to save money, but why would you? The returns to performance are even higher in the workplace, which drives pricing power.

In this mental model, the frontier labs as businesses, will look like new, reimagined forms of a mix of Apple and Microsoft. The Apple side is that they’re selling an integrated, extremely hard to replicate technology. The Microsoft side is selling high-leverage subscriptions across the economy. In 5-10 years I expect both OpenAI and Anthropic to be valued in the $2-10T range. The true frontier labs will be an oligopoly that looks like the cloud market today.

On the other side of this equation is the open model economy. This isn’t to say that the frontier labs will dominate all aspects of AI use. Yes, I expect OpenAI and Anthropic to be the most representative companies of the AI boom (new companies, alongside Nvidia of course), but the collective value capture around open models will be far bigger overall, it’s just that the revenue and margins will be shared across a wide stack of companies.

Many businesses want to switch to open models but the models today are not good enough in out-of-distribution tasks. Eventually open model builders will stop chasing Claude and GPT on the Artificial Analysis index and fill this niche. This fork could be driven by economic factors, where they no longer have the revenue to support the growing R&D costs for continuing to scale models. It can also be driven by pure demand, where certain AI solutions only can exist at low price points present in open models. Where closed labs are an oligopoly, open model builders and users will be far more diverse and numerous. The total market value will dramatically exceed the cumulative value of OpenAI and Anthropic.

Open models are by their nature not integrated, so they will rely on multiple companies coordinating to serve them. Each of these layers will have alternatives, driving prices down to commodity pricing. These low, predictable prices will be where many enterprises enter to build in-house agents and tools for niche tasks. The predominant mode of deployment here is that enterprises find a model that hits a sufficient performance threshold on a task of interest and does not replace the model later (setup costs are high). As customizing models becomes easier, again in the open model finetuning stack we are seeing emerge (Tinker, Fireworks, Prime Intellect, etc.), this market becomes even bigger.

What this will look like in the coming years is a steady rise in open model inference proportion across the entrenched hyper-scale clouds of Google, Amazon, Microsoft and new AI infrastructure companies of Together, Fireworks, OpenRouter, etc when compared to OpenAI and Anthropic.

The closed models hit incredible product-market fit with the current agents, starting their integrated exponential by monetizing the top end of the knowledge work. The open model economy will take far longer, but it will also be far more satisfying to follow, as it tracks the broader diffusion of AI into the entire economy and world.

1

The term coding agent is funny because we barely write code in them. They’re general agents that are so capable because they write a lot of code.

Liking, sharing, commenting, or recommending Interconnects from your Substack is the only way Interconnects is possible. Thank you for your support.

If you liked this, consider upgrading to a paid subscription to cover my growing subscription and API fees. We offer group Interconnects subscriptions at tiered discounts for 5+ heads.

If you want all of the best AI writing on Substack through one subscription for your team of 20+, check out https://readsail.com/.

Americans pay more for healthcare than any country on earth — and they're getting less for it every year.

In this week's Prof G+ Deep Dive, Scott explains why hospital consolidation is the real driver of America's healthcare cost crisis, what solutions actually exist, and what's standing in the way.

If you’re not a Prof G+ subscriber yet and want access …

No ads on pods, because ads tax your most valuable asset: time

Prof G+ exclusives, including breaking livestreams, deep dives, keynotes, and more

Community privileges to leave comments, make friends, and engage in a series of bad decisions that might pay off

Drake Dukes · Monday, June 1 2026 · 7 min read · ↑ top

Former Apple Siri & Roblox ML scientist enters stealth, Ex-Ogilvy PE operator builds AI for the full PE deal lifecycle, & Ex-Lyft hardware director exits stealth with $12M to test hardware in seconds

We’re tracking company launches as they happen and surfacing the most interesting new founders and startups (yes, all outside of this stealth activity too). If you want to stay ahead of the curve, this is where you’ll find them first.

Right now we’ve got 5 subscribers: my wife, my mom, and that high school buddy who won’t stop pitching me his app. Be smart like them and get in early 👇

We run a live feed inside Gravity that tracks founders entering stealth and companies quietly exiting it.

What you’re reading here is about 1% of the stealth activity we pick up. The full tracker updates in real time as things change and new activity emerges.

Co-Founcer & Co-CEO:Maximiliano Casal(Co-Founder at Nowports - YC W19 unicorn)

Arkimedes is an AI infrastructure platform for private equity firms, offering five integrated modules covering the full deal lifecycle built for large-cap PE, mid-market PE, and corporate development teams.

HQ: New York, United States

Industry: FinTech, Private Equity, Enterprise AI | Team Size: 8

FounderDNA: Serial Founder, Top 10 University, Masters Degree, Doctorate Degree

Prior Experience: Data Scientist at McKinsey & Company, Computational Biologist at Harvard Medical School, Co-Founder & CEO at Expand Consulting, Co-Founder, ML at Maka Media

Prior Experience: Security Team Lead at Axis Security, Cyber Security Researcher at Rafael Advanced Defense Systems, Security Research & Development at Israel Defense Forces

Ocean is an agentic email security platform that uses purpose-built AI agents to detect malicious intent in targeted and novel email attacks, replacing legacy pattern-based detection with context-aware analysis at enterprise scale.

HQ: New York, United States

Industry: Cybersecurity, Email Security, AI | Team Size: 2

Latest Funding: $28M Series A Round on 5/19/2026

Key Investors: Lightspeed Venture Partners, Picture Capital and Cerca Partners

FounderDNA: Serial Founder, Technical Founder, Masters Degree, Doctorate Degree

Prior Experience: Director of Hardware Engineering at Lyft, Head of Electrical Engineering (Jump) at Uber, Director of Engineering at Flex, Co-Founder/Director of Hardware Engineering at Olio Devices

Panacea pairs experienced ex-FDA regulatory consultants with an AI platform to deliver the fastest and lowest-cost pathway to FDA approval, offering fixed outcome-based pricing across all major regulatory pathways.

HQ: San Francisco, California, United States

Industry: HealthTech, Regulatory Technology, Biotechnology | Team Size: 2

Time Spent in Stealth Mode: 5 Months

🕵️♂️Key Talent Going Under Stealth

Illuminating clues left behind by world class talent and influential innovators who just went into stealth mode

Mahesh Nandwana - Founder at Stealth Startup

FounderDNA: Technical Founder, Masters Degree, Former FAANG

Prior Experience: Technical Lead/ML Scientist (Siri Perception) at Apple, Senior Principal ML Scientist (Foundation AI) at Roblox, Advanced Computer Scientist (Speech Technology and Research Lab )at SRI International

Co-Founder and CEO:Mark Miller (General Manager and Head of Product - Business Prime at Amazon)

HQ: Seattle, Washington, United States

Time Spent in Stealth Mode: 1 Month

Kyle Morgan - Founder at Stealth AI Startup

FounderDNA: Former FAANG, Top 10 University

Prior Experience: Lead UXR (Bard & Gemini) at Google DeepMind, Lead UXR, Applied AI / Enterprise AI Agents at Google, Head of Digital Experience at Vocus Group Limited, UX Design Research Manager at AGL Energy

Vera Chichagova - Co-Founder & CEO at Stealth Startup

FounderDNA: Masters Degree

Prior Experience: Director Regulatory Compliance at OKX, Group Head of Regulatory Compliance at Revolut, Vice President Compliance at Barclays Investment Bank

🚨Here’s the deal 🚨This email has gotten too big. Exciting, but with more people following it, the edge diminishes. I’ve thought long and hard about what to do to preserve the value in the signals. I’m not sure about the final direction yet, but in the meantime I’ve been sending an email 48 hours earlier to a select group of paid subscribers. The feedback has been pretty positive so I’m going to open up the list for another 100 spots. To get signals early, Apply here!

Stay Stealthy,

Drake

Thank you for reading. If you liked it, share it with your friends, colleagues and everyone interested in staying ahead of the hidden developments in tech. Subscribe below and follow us onX / Twitter to never miss a company operating under stealth again.

Stealth Startup Spy is a data-driven newsletter for investors, journalists and tech enthusiasts interested in uncovering the next big move for key talent, real-time stealth company launches and technology advancements not in plain sight. We leverage the technology built at Gravity to shine a light on the hidden world of stealth startups.

Scott Galloway · Tuesday, June 2 2026 · 2 min read · ↑ top

Plus, the Markets Tour is live from NYC… tonight

I foster a decent amount of loyalty among the people I work with. It’s not a function of character or empathy, only the recognition that nothing wonderful happens when you’re on an island. Greatness is in the agency of others. Behind my bold predictions, sharp analysis, and smart takes there’s a talented research team, led by Mia Silverio. Extra Credit is a newsletter where that team steps into the spotlight.

Each week, Extra Credit brings you one new story that digs deep into a business or business-adjacent topic that isn’t aggregating attention — but should be. Every post also includes a page from the Prof G Media storytelling playbook, with the writer sharing the narrative techniques we frequently deploy. It’s a twofer: Get smarter, become a better storyteller.

Since you’re already a Prof G subscriber, you’ll automatically receive the free Extra Credit posts, but if you want the all-access pass you’ll need to upgrade here. Or, you can make a bad decision, i.e. opt-out by clicking here.

First post drops tomorrow. Enjoy.

Students Eat Free

Well, not quite free, but we’re celebrating the launch of Extra Credit by offering 50% off annual and monthly Prof G+ subscription plans to students and educators with an academic email address. Matriculate below (or share with your favorite student).

Live from New York

… it’s Tuesday night!

That’s right, we’re livestreaming the sold-out final stop on the Prof G Markets tour from NYC tonight at 7:30 p.m. ET , exclusively for Prof G+ subscribers.

Love listening to me and Ed Elson on Markets? Tune in, we’re even better live. Love the Mooch? Tune in, Anthony Scaramucci joins us onstage as a special guest.

Still not enough for you? Maybe our surprise guest will move the needle. I’d say who, but I’ve been briefed on why keeping things under wraps is a matter of national security (seriously). So, yeah… they’re kind of a big deal. Curious? Join us tonight at the link below.

Raging Perspective

Last week, we debuted Raging Perspective , our Substack-exclusive live show brought to you by my Raging Moderates co-host, Jessica Tarlov, and Gen Z political analyst, Aaron Parnas. Watch a replay of the first episode in all its unscripted, unfiltered, unedited glory here.

Raging Perspective is back again this Wednesday at 2 p.m. ET (note the time change, this week only). Register below to be notified when the stream goes live, and don’t forget – this show is interactive, baby. Bring your rage, and your questions.

See you tonight on the Prof G Markets tour livestream.

ben's bites · Tuesday, June 2 2026 · 6 min read · ↑ top

NVIDIA and Microsoft birthed a new computer

Hey folks,

I’m spending as much time as possible off Twitter, and any other general doomscroll distractions. I’ve got work to do (the course/manual/whatever it’ll be called).

Aiming to get at least the preview ‘lessons’ out this month.

I’m not going to force any wisdom out in today’s intro because it’s not my style.

Pulse is world’s fastest speech-to-text model (#1 on Sierra’s μ-Bench for P95 latency) with top performing accuracy (under 5% WER on Artificial Analysis leaderboard), works across 39 languages and 100+ accents.

Get $25 free credits, use code BYTE25-N3CX3UKV (valid till 6/6)

Headlines

Claude Opus 4.8 is out, with dynamic workflows in Claude Code. Claude now writes an orchestration script, then spins up subagents in parallel to work through complex tasks.

Dex’s take: this doesn’t prove loose multi-agent systems work. Deterministic workflows around small agent loops are more reliable.

Claude Opus 4.8 - Simon Willison calls it a modest but useful upgrade, mostly because it’s more honest about uncertainty and less likely to miss flaws in its own code. Every’s vibe check is more bullish: they found it a big jump from 4.7, strong at coding/writing/knowledge work, and competitive with GPT-5.5 on their internal senior-engineer benchmark. The catch is the harness: the model is back, but Claude’s app still feels messier than Codex.

Stacker's AI Accelerator is offering $500k in inference credits to businesses ready to go AI-first. Selected companies get credits and hands-on mentoring to deploy AI agents across their operations. Applications close June 9th. Apply now.*

My feed

Stacker is an AI coworker that joins the dots in your business. Stacker lives in Slack, connects your tools, and does the work.*

Emil Kowalski

@emilkowalski

To get good animations from an AI you need to get good at telling it what you want: - "stagger this list of items" - "make this animation direction-aware" - "spacial consistency", "crossfade", "layout animation", I made a motion vocabulary for this: animations.dev/vocabulary

Wes Winder

@weswinder

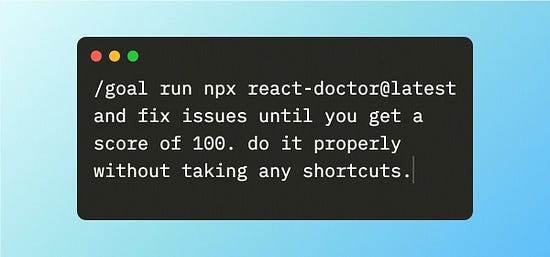

this codex prompt is literally the best thing ever if you are building react apps and want the cleanest possible code simply run "/goal run npx react-doctor@latest and fix issues until you get a score of 100. do it properly without taking any shortcuts" in codex thank me later

Lenny Rachitsky

@lennysan

My biggest takeaways from @benedictevans : 1. We’re in 1997 for AI—it’s as big a deal as the internet or mobile, and only as big a deal as the internet or mobile. We’re at the stage where most stuff kind of doesn’t work yet, most of what people will build hasn’t been built, and

Lenny Rachitsky @lennysan

A rational conversation on where AI is actually going with @benedictevans For 20+ years, Benedict has been one of the clearest, most reliable thinkers on where technology is heading, and how it'll impact our lives. He was @a16z's resident "thinker" for 5+ years, and has spent

Farza 🇵🇰🇺🇸

@FarzaTV

Watch me control my computer with just my voice. This is the future of operating systems. No hands. GPT-Realtime 2.0 is very, very underrated. Demo:

Interconnects by Nathan Lambert · Tuesday, June 2 2026 · 15 min read · ↑ top

Listen to post · 15:50

I’m departing the Allen Institute for AI (Ai2), where I got the great privilege to work on the Olmo models, to grow, to learn, and to have broad lasting impacts. This post is an attempt to reflect on why what we did was influential, despite obviously being far from the frontier in performance (even when within size buckets), and how this reflects on various paths to impact in AI today.

To start, I shared the following note with the company yesterday:

Dear Ai2.

As many of you know, today is my last day working at Ai2.

I joined Ai2 largely as an accident. I met Luca at ICML 2023 in Hawaii and realized I could level up my open post-training work dramatically if I got the chance to join. When I got an offer it was an absolute no-brainer, it was such a welcoming and exciting environment.

It has been a wonderful ride that has transformed my life, and I couldn’t be prouder of the work we did together. Ai2 has a wonderful scientific culture at its core and I’m excited to see this continue. I feel very lucky to have been here and that I personally have benefited massively from everyone who has worked so hard to cultivate that culture and environment. It is and has been a team effort. This includes all the people whose longest interactions with me were brief chats at the coffee machine. I drew so much energy and excitement from all the different ways people at Ai2 showed up for the mission.

I’ve already thanked much of the OE team directly, but I wanted to thank everyone else that went into this. Legal, IT, Comms, and the Office team all do a great job enabling and leveling up our research work. It’s often work that is forgotten, outside of the lime light, or remembered at the last minute, but it all has been crucial to achieving our goals. I’m excited to keep visiting the wonderful Northlake space in the coming years.

Even though I’m leaving, I’m more excited than ever about Ai2’s mission. Ai2 operates in such a rare niche between academia and industry, where we can explore and influence the most important technology of our lifetime. Doing this openly is the best way to ensure the technology diffuses safely to everyone who may benefit. Ai2 needs to stay as ambitious as possible, trying to influence the cutting edge of AI and the biggest issues of the field. Do not shy away from these challenges – AI needs independent voices as it only becomes more geopolitical, socially disruptive, and central to the economy.

I will still be working in this space, working to make the open ecosystem better coordinated and more useful.

So as I go off to try something new, don’t be strangers. I’ll always be reachable at nathan@natolambert.com and will still live in Seattle for most of the year.

Nathan

I have loved and will still love Ai2. Ai2 has a deep culture of caring about the research process, the outputs that get shared, and most importantly the people who do the work. This is why the institution creates countless wonderful people that go and spread the gospel throughout the research community. This core culture will remain through the rebuild, and there are plenty of resources to do impactful research across the spectrum of AI.

In the last two years of my time at Ai2 I’ve done so much meaningful work. Of course Olmo is at the top and has been my priority, but making time for consistent practice here on Interconnects, weekend cram sessions for ATOM, and also the fun RLHF book make for a list that makes me wonder how I did it all. I was obviously obsessed with work, but not in a way that made me lose sleep or lose my overall wellness. It was the right long-term approach.

This impressive list is one where I was ruthless in saying no to things that didn’t matter and got all my work out to see the light of day. I had no medium-sized projects that didn’t succeed in the last few years. It makes me wonder if I wasn’t taking enough risk. It shows you can truly do so much with your time, and it’s actually harder to find the right problems and environment to do it. Many people are in environments where their work never becomes public or they’re forced to change topics consistently.

From zero to hero

To start, I’d like to do a short recap on my path to Ai2 to show what Ai2 was just as much a growth story for me as an execution story.

I studied electrical engineering in undergrad, focusing on linear systems math and microelectronics.

I was admitted to the UC Berkeley EECS Ph.D. program to study microelectromechanical systems (MEMS).

I showed up at Berkeley in August of 2017 and realized AI was obviously the thing I should be doing. I asked the likes of Sergey Levine or Pieter Abbeel if they could advise me – they said no.

I threw all my energy into learning what I could about AI. I got a break to get advised by one of Sergey’s post-docs in 2018 or 2019. I went all in on that, I fought for funding, I fought to have an AI paper.

This process worked out by the end of my Ph.D. in 2022: I had access to the Berkeley AI Research (BAIR) building and collaborations in the department. It was a bumpy road.

I wanted to go to industry research, to get a nice paying job with intellectual freedom, something like FAIR or Google Brain at the time. HuggingFace was the only job that fit that bill, it was easy to say yes to.

I joined HuggingFace in May of 2022 and wasted my time at the company until ChatGPT was released. I used my RL background to write a blog post on RLHF which went viral. HuggingFace decided it would be good for me to form a team around this success.

In 2023 I learned NLP and about language models. I had a lot of fun and built an initial community. I got burned out by working remote with a huge time difference. I met Luca Soldaini at ICML in Hawaii, where I was giving a tutorial on RLHF, and they told me Ai2 was hiring.

I got the job at Ai2 largely because of my excitement and how I was saying I wanted to do a lot of stuff that sounded cool to them but no one was likely to do (RL related things). My interviews were far from a sure thing – this is a great job to land!

I started at Ai2 in October of 2023. I worked remotely for a while. I was doing normal research, I made the first reward model evaluation, RewardBench. It was a solid success, but nothing like how the pretraining team was getting ready to release the first Olmo.

I helped coach Ai2 on how to release models well, helping the Tülu 2 project land (the first model to do DPO well, publicly at the 70B scale).

The first Olmo was released in early 2024, I squeaked onto the papers just by trying to be helpful and doing some basic post-training. I was already good at paying attention to which projects are actually important.

That summer I started rounding everyone up to do a “big frontier post-training project.” This became Tülu 3, one of my favorite projects ever released, in fall of 2024. The goal was to beat Llama 3’s post-training with their own base model. The team morale was incredibly high and the execution was so timely, allowing us to coin the term Reinforcement Learning with Verifiable Rewards (RLVR) in the paper.

The crazy lengths I went to get the Tülu 3 and Olmo 2 post-training done had me sending 40% more slack messages than anyone at the company and got me the award “The Cat Herder.”

2025 was a much simpler year. We were too slow to react to reasoning models, given we had been doing similar stuff with Tülu 3, but sometimes that happens.

Originally we wanted to release Olmo 3 by June or July of 2025. That obviously didn’t happen, but we got the slim chance to train a bigger model, and it really landed. We threaded the needle.

Since Olmo 3 was released, it was clear that some changes were coming and I personally never got a big post-training project off the ground after that. Many other people managed great work in the spring of 2026.

This all leaves me here today showing you that only about half of my story at Ai2 is what I was known widely for, and the rest was building momentum. It often takes a year of building relationships and direction before really big successes can happen in a career.

I was just about a nobody when I joined Ai2 and I got to join a team that was willing to learn from the skills I had brought from HuggingFace. With how media works, I often think I get more recognition than I deserve for Ai2’s success.

The likes of Tülu 3, Olmo 2, and Olmo 3 felt like generational team efforts. The amount of personal successes and breakthroughs that happened for those projects is immense – and to sustain them over such a long time period is incredibly hard to replicate. The sum far exceeded the individual parts.

I’ve heard many times in the last few months how people wouldn’t know about Ai2 if it wasn’t for my writing. Statements like this are overblown, but they are partially true and reiterate how crucial building relationships and getting the word out is today.

When you write a plan that is feasible, the world bends towards that plan. When you convince people it’s going to happen it only becomes more likely. Vision and compelling explanations are one of the items in shortest supply in the tech industry. Often building the thing is easy and explaining it is hard. If no one knows about your work, the value is often close to 0. So much of building reputation is about building relationships with people who will receive your work.

Reflecting on all of this, I’ve had a shockingly linear path through my career to incremental success. I would expect the first 10 years of most careers to be in search of finding one opportunity as good as Ai2, and you will not always be able to seize it. There are some ways to create more opportunities.

I’ve discussed before how a large part of my rise is down to many more senior and more established scientists being drawn into the closed ecosystems at the same time as an immense swell in interest for AI. This created a power vacuum that I, and a few other prominent scientists that I think form my “generation”, got to grow rapidly into.

The role of public scientists

With my work at Ai2 and Interconnects, I summarize my role and mission as trying to accomplish three things:

Provide clarity in the evolution of frontier models. This is easiest when the science has caught up, but even applying a scientific lens to how the models are changing is very useful to building trust in the broader AI ecosystem.

Create a vibrant and diverse open (model) ecosystem. This is crucial to mitigating some risks of AI, particularly with concentration of power and myopia in studying frontier safety, that has motivated me now for 3-4 years. The risks haven’t abated.

To build institutions that create people and ideas that further the above missions, and generally mission-driven individuals that are willing to advocate and build a future they believe in. AI is a grand problem, and not one that I can do alone, so I need to build brands to rise through the noise and attract likeminded people.

At my best, I have many avenues for impact. I help open researchers work on impactful problems – not wasting the precious compute and time they have during the AI boom. I help policymakers know what is true. I build models that people use. I tell stories that make people smile. I keep the list wide so that I can stay motivated.

I see all of this continuing, and have been thinking about the broader impacts of this repeatedly over the last few months. Hearing that Andrej Karpathy was joining Anthropic prompted me to finally share more of my opinions:

For a long time, academic researchers being at the cutting edge of new technologies has been a great social equilibrium. Neutral, unbiased technologists have been the people to spread new ideas to the world.

As AI research takes off in velocity, it is also going behind closed doors. The tech industry has sowed distrust, and now they are the ones trying to tell the world about incredible changes coming. It’s a big loss to a form of social contract in America.

There’s been a history of scientists helping society understand new technologies. There is a public service in the culture of science that I want to see continue.

It’s being exacerbated by feelings of FOMO, especially financially driven, where I’m seeing many people who previously wanted to be professors -- and likely still do deep down -- feel a need to conform and chase money, in a pocket of industry. I get it, I grapple with this.

For those with a safety net, there will be great returns to some who choose to zag, and try to build something good, for people who need something different. For me, this is building interesting, fully-open models, to show what you can do with a variety of open weight sizes.

Yes, AI’s immediate future is dictated by the frontier, but it’s long-term trajectory still deeply includes academic institutions and open science. Knowledge will always diffuse, but to whom?

As of today, I think China is positioned to be the global home of AI research in a few years. The home of research is where ideas are accessible, spread rapidly, and are nurtured. The U.S. seems to be unwinding many institutions and relationships.

The largest returns go to people who build something differentiated, at least in reputation, and a lot of people are not being shown that this path exists.

To elaborate on this, I don’t fault any of the individuals who are going to industry today. I’ve been very close to doing this myself in the past weeks of job searching, or rather job exploring. It’s a systematic problem where scientists cannot easily get the support to take bold stances, especially stances that are designed around the public good.

To go a step further and say that only the research within closed, frontier labs matters is very myopic. Yes, there’s a sort of research you can only do with vast compute resources, and they will directly impact the most revolutionary tools of the day. But, I see the relative opportunity to do good elsewhere as higher for plenty of people.

Open research will always be the standard that sets the language people use to understand AI. It’ll always be how the next generation is trained – even if it’s behind what industry has built. It’ll be the ecosystem where new long-shot ideas are built. Without investing in this open ecosystem, all of these cycles will be kneecapped.

At the end of the day, so much of my role now is just showing the path to impact in this domain. To show how clever, mid-sized open models can impact real problems in the world. To show how policy-makers and educators need open research to structure the rest of society around AI. This is a fun role too! It would be very sad for me to see this light diminish ever further, into the lightest embers of a fire that looks almost entirely out.

Even if the pace of research were to slow further, if the folks remaining like myself got financial offers they can’t refuse for their families’ sake, the torch of open research will never fully go out. It’s core to how science is taught and done. There is a next generation coming, they just look for guidance and role-models.

What’s next

I see the best Ai2 work as research infrastructure. Building recipes in public gives countless researchers the ability to ask very specific questions of training processes. We need these researchers in the broader community, as Ai2 could never answer all the interesting questions themselves. One of my great joys in recent months has been visiting a top ML university and hearing so many graduate students say they’re building on Olmo. This is how the world should work!

Going forward, I still plan to operate in similar spaces, fighting for open-science, imagining what the future of the open model ecosystem can be, and doing my best to make the social transition to an AI-native era smooth. I’m most excited by how you can train medium sized open models on specific tasks that become useful tools in complement to the frontier models – massively winning on price. I want to invest in the ecological diversity of open models and coordination across builders.

For something that isn’t surprising given my past focus areas, I’m watching the pace of releases from all labs open & closed, and how they’re hillclimbing on super ripe new post-training veins (on-policy distillation, agentic workflows, etc.), it’s clear that fully-open post training recipes are about as far behind as they ever have been & falling further behind. I’d like to fix this. It’s not 100% clear yet if I will this year, but I’ll try.

To do this best and to execute, mostly personally, I needed a new start and fresh perspectives. I’ll be carefully building what I’m doing next over the next few months and am eager to share more about it when I can. One of my close teammates at Ai2 shared this quote with me in a farewell card, and I found it very apt in where I’m going next.

The object of life is not to be on the side of the majority, but to escape finding oneself in the ranks of the insane. — Marcus Aurelius

Liking, sharing, commenting, or recommending Interconnects from your Substack is the only way Interconnects is possible. Thank you for your support.

If you liked this, consider upgrading to a paid subscription to cover my growing subscription and API fees. We offer group Interconnects subscriptions at tiered discounts for 5+ heads.

If you want all of the best AI writing on Substack through one subscription for your team of 20+, check out https://readsail.com/.

A guide for identifying which state of AI adoption matches your needs, complete with sample prompts and advice for when it’s time to move to the next level

by Mike Taylor All it takes is one viral post to make you feel like you’re using AI all wrong. Someone’s running 12 Claude Code sessions in parallel. Someone else’s agent answers emails while they sleep. Meanwhile, you’re still arguing with ChatGPT. Here’s the thing: Keeping up with the power users isn’t the point. The best way to get value from AI is to use it in a way that fits your work—and to check in now and then to see whether you could be getting more from it. With that in mind, today we published a guide that maps all eight levels of AI adoption, from chatbot basics to full agent orchestration. We explain how each level works in practice, with sample prompts, so you can figure out which ones match your current needs and workflows, what’s possible at each stage, and when it’s time to move to the next one.

Level 1—Chatbot: You ask, it answers.

Level 2—Copilot: The AI works alongside you, inside your files.

Level 3—Agent: It executes a task step by step, checking in for approval.

Level 4—Autopilot: It runs on its own; you review the result.

Level 5—Workflows: You build a system that makes its output more reliable.

Level 6—Assistant: It works in the background, without being prompted.

Level 7—Multi-agent: You manage several long-running agents at once.

Level 8—Orchestrator: A manager agent runs a team of sub-agents for you.

A higher level isn’t necessarily better. The right level for a task is generally determined by how much you trust the AI to do a good job without intervention, and how big a deal it’ll be if it does mess up. If you want to know where you fall on the AI adoption spectrum—and whether it’s time to experiment with higher levels—this guide is for you. Read the 8 levels guide

Prof G Research Team · Wednesday, June 3 2026 · 7 min read · ↑ top

The autonomous vehicle rollout is about to get a lot more complicated

Every year, more than 36,000 Americans die in car accidents. Compared with human drivers, Waymo’s autonomous vehicle (AV) technology results in 92% fewer serious accidents, suggesting it could prevent many of those deaths. But after a year of the company operating eight cars with zero accidents in New York City, Mayor Zohran Mamdani let Waymo’s testing permit expire anyway. When asked why at a press conference, Mamdani made his position clear:

“Look, if a company like Waymo finds itself in New York City, what they will also find is a City government that is committed to delivering for the workers who keep the city running, and those workers also include our taxi drivers who, for far too long, have been sold a dream of being able to work their way to the middle class, only to have the rug pulled out from under them.”

To translate: The mayor of New York City will not let technology companies automate the work of taxi drivers and rideshare drivers. He won’t be the last politician to take that stance.

Hit the Brakes

For as long as autonomous driving has existed, there has been organized resistance to it. Mamdani is not an outlier — he’s the latest and most prominent face of a movement that has been working for nearly a decade to slow, stall, or stop autonomous vehicles from replacing human workers. That movement has a name, a headquarters in Washington, D.C., and 1.3 million members: the International Brotherhood of Teamsters, America’s largest private-sector union and the most powerful force standing between autonomous vehicles and the open road.

Nearly a decade ago, the Teamsters successfully lobbied Congress to exclude autonomous semitrucks from legislation that paved the way for autonomous vehicle testing. Four years later, in 2021, they shut down a bill that would have relaxed federal autonomous vehicle rules. In 2023, the Teamsters backed a California bill that would’ve required human drivers in all autonomous trucks. The bill made it past the state Legislature, but Gov. Newsom vetoed it.

As autonomous driving develops into more serious technology, so do the Teamsters’ efforts to halt it. Last year, the conflict intensified when Teamsters Local 25 called on Waymo to pause their planned Boston rollout altogether.

“Waymo is steamrolling into cities throughout our country without concern for workers or residents,” said Local 25 President Tom Mari at a rally outside of Boston’s City Hall. “They’re doing this because they want to make trillions of dollars by eliminating jobs.”

As of now, Waymo is continuing their testing in Boston despite the Teamsters’ opposition. Under the current Massachusetts permitting process, all autonomous vehicles need ahuman operator behind the wheel. There’s currently a bill in the Massachusetts State House that would change this — but it’s been met with a competing Teamsters-backed bill that would officially codify the requirement for human operators. It’s unclear how or when this conflict will be resolved, especially as Waymo continues to ramp up its lobbying spend.

What is clear, however, is that these legislative battles are not one-off events. They’re the beginning of what will be a long path to seeing autonomous vehicles on the roads of all 50 states. And for good reason — the Teamsters have a point. Job destruction is coming.

Driver Destruction

Since ride-sharing services began popping up in the early 2010s, they’ve become the backbone of the gig economy. According to Deloitte, about a third of the American workforce participates in the gig economy. From there, it’s estimated that at least a quarter of American gig workers drive in some capacity, whether that be delivering food, groceries, or humans. Autonomous vehicles put all of these jobs at risk.

If we zoom out to include other driving occupations, it gets even worse. According to the Bureau of Labor Statistics, there are roughly 440,000 taxi and limousine drivers, 460,000 food delivery drivers, 1.5 million small-package delivery drivers, and 2.2 million long-haul truckers. That’s a total of 4.6 million jobs.

Driving is also the most common occupation among young men without a college degree, by far. All of this means that, as you read this, nearly 3% of the American workforce is in the crosshairs of Big Tech.

Nearly all of those occupations are, in some capacity, represented by the Teamsters union. The transportation sector as a whole has a union penetration rate of about 14% — a minority, obviously, but still more than double the rate of the private sector in total.

The Teamsters’ fight against autonomous driving is important not only to its members but also to its very existence. If the Teamsters begin bleeding members due to automation, they’ll start losing dues, which would place pressure on the union’s finances and dampen its political influence.

Outside of unions, it can be assumed that there will be plenty of political capital to be gained in future elections for politicians who choose to take a stance against Big Tech and autonomous vehicles. The tide is turning on all forms of AI, and public polling already reflects this reality.

The share of Americans who think AVs improve road safety has actually fallen 12 percentage points since 2018 — and that’s despite the technology becoming exponentially safer over the same period.

Compared with human drivers, Waymo vehicles have 82% fewer injury-causing crashes, 92% fewercrashes involving injured pedestrians, and 85% fewer crashes involving injured cyclists. Last year, car accidents were the leading cause of death for Americans ages 5 to 29. In an entirely Waymo’d world, more than 33,000 lives would be saved annually. But without public buy-in, none of this matters.

The raucous boos at graduation ceremonies across the country illustrate how unpopular artificial intelligence and autonomous technologies more broadly are in America. Autonomous vehicles are possibly the most visceral andphysical embodiment of AI that the average American might interact with on a regular basis. In cities where Waymo or Tesla or Zoox operate, autonomous vehicles are everywhere. They serve as a constant reminder of the once-farfetched, unrecognizably transformed future that awaits us — a future that most Americans interpret as dystopian.

Let’s Talk

The Teamsters are not the first union to stand in front of automation. In the 1810s, English textile workers — the original Luddites — smashed power looms with hammers in the dark of night. In the end, it didn’t save their jobs.

A century later, elevator operators’ unions fought to keep humans at the helm of automatic elevators. Those jobs are long gone. In the 1960s, longshoremen’s unions battled the introduction of shipping containers. The longshoremen lost that fight, but not before negotiating severance funds and job guarantees that softened the blow for existing workers. The pattern is undefeated: Technology always wins, the only question is how much protection workers are able to take with them on the way out.

This is exactly why Mamdani and the Teamsters are wrong. Letting the permit expire is not good for labor — in fact, it has the opposite effect.

The more honest and useful fight is the one the longshoremen eventually settled for: not blocking the technology altogether but demanding that the companies deploying it bear some of thecost of the disruption they’re causing. Retraining funds, transition payments, even a Waymo-funded safety net for displaced drivers are all policies worth proposing. Instead, the Teamsters’ current Luddite-inspired strategy will leave workers empty-handed. The question they should ask themselves is: Do you want to be right or do you want to be effective?

Each week, this section will give you an inside look at how this article came about, as well as the analytical and storytelling techniques the author used to report it.

Working with Ed on Markets has made me acutely aware of the public’ssouring perception of all things artificial intelligence. Months before commencement speakers were getting heckled for mentioning AI, Ed pointed out the mounting opposition to data center construction across the country and its relation to politics.

I’ve been following the autonomous race closely, and Ed’s findings made me wonder: Is the same thing happening with robotaxis? I realized that the answer was a resounding yes. But when you think about thetrade-off between safety and jobs, things get complicated … and a lot more interesting.

One more thing: Part of being a good analyst is recognizing patterns across different domains. When a new story reminds you of something you’ve seen before, follow that instinct. History might not always repeat, but it’s always instructive.

Dan Chiolan is a research analyst on the Prof G Markets team. He started as an intern in 2024 before joining Prof G Media full time after graduating from Temple University.

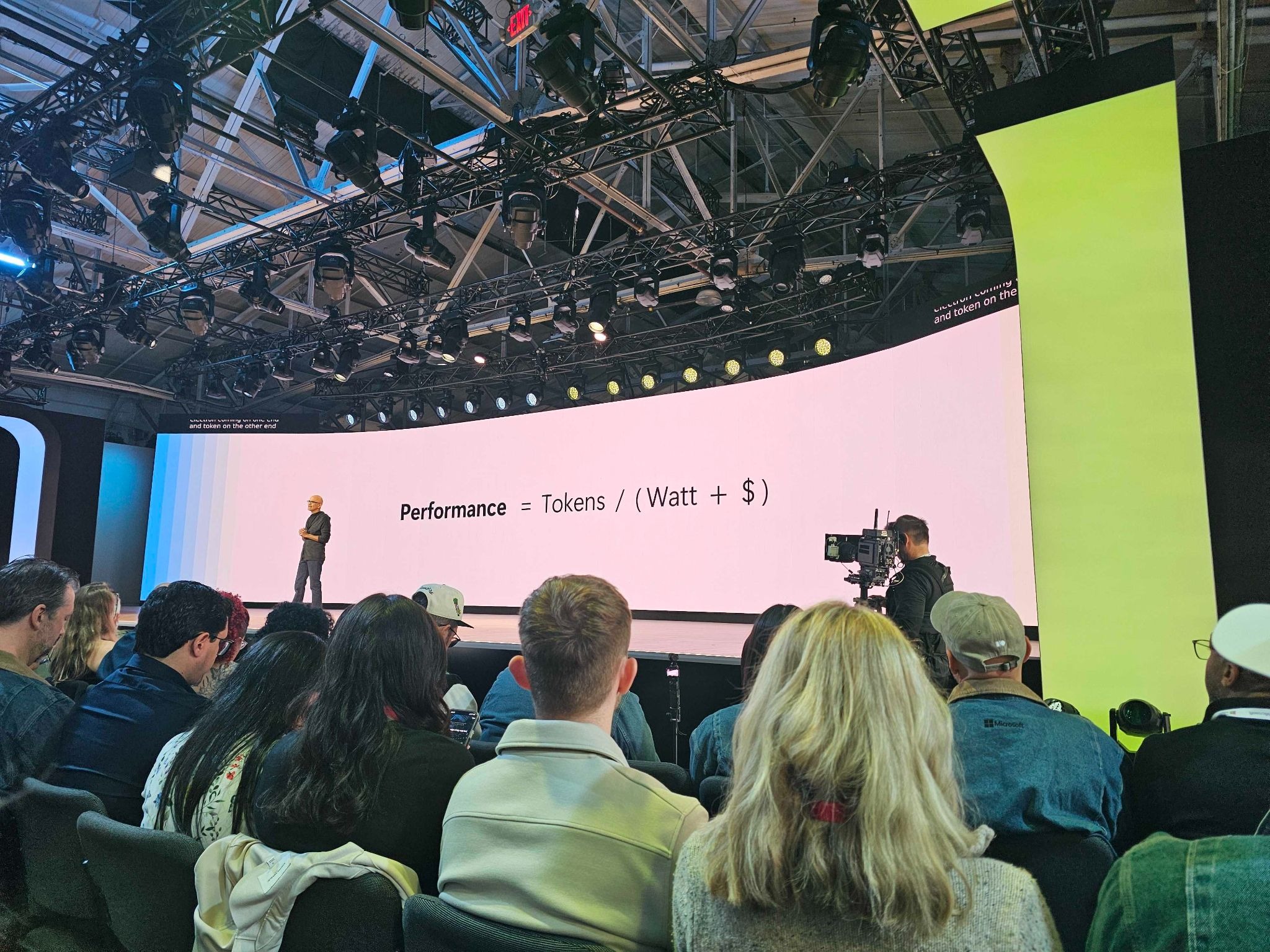

Yesterday Microsoft added a new metric to a model release card, one that will likely become a standard.1 Average token usage. In the first row, the Microsoft model hits 71.6 on SWE-Bench Verified using about a third of the tokens Claude Haiku 4.5 burns. Benchmarks are now measured on two different dimensions, the overall performance & the cost to achieve that intelligence. This is yet another sign that the era of subsidies2, tokenmaxxing3, & all-out performance for many use cases is over. Even the most valuable companies in the world cannot afford state-of-the-art intelligence for every conceivable use case.4 Uber capped employee AI spending after blowing through its budget in four months.5 Salesforce is spending $300M on Anthropic tokens & has frozen engineering hires.6 This new dual benchmark answers the buyer’s only question : what is my intelligence per dollar? Artificial Analysis already benchmarks this.7 GPT 5.5 & Claude Opus 4.8 land within a point of each other on the Intelligence Index, around 60. Running the index costs $3,357 on GPT 5.5 & $4,685 on Opus 4.8. Same answer, 40% more expensive. Model companies must now compete on both dimensions. The application layer will compete one level up, on dollars per outcome, what a closed ticket, a shipped PR, or a resolved support case actually costs. Every layer in the stack now has to price the same way the customer thinks : per result, not per token.

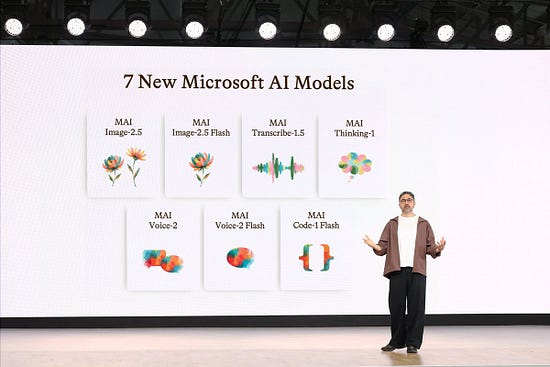

1. Introducing MAI-Code-1-Flash — Microsoft announces a new coding model with average token usage on the release card. ↩︎

2. The Unsustainable Subsidy — The era of AI subsidies is ending. ↩︎

3. Tokenmaxxing — Models that game benchmarks with extra tokens are losing their edge. ↩︎

4. Microsoft cancels Claude Code licenses, shifting developers to GitHub Copilot CLI — Microsoft cancelled Claude Code licenses across its Experiences and Devices division (Windows, Microsoft 365, Outlook, Teams, Surface) after engineering usage outran budgets. ↩︎

5. Uber caps employee AI spending after blowing through budget in 4 months — Uber caps employee AI spending after blowing through budget in four months. ↩︎

6. Salesforce Spends $300M on AI, Freezes Engineering Hires — Salesforce Spends $300M on AI, Freezes Engineering Hires. ↩︎

7. AI Model & API Providers Analysis — Independent analysis of AI model costs. ↩︎

A year ago, USV decided to explore what an AI native VC firm would look like. We hired Spencer who built a platform and a bunch of agents and wrote this post about all of that before departing to do a startup. And we paused our longstanding analyst program last year and saw how far we could get with agent analysts instead of humans analysts.

ben's bites · Thursday, June 4 2026 · 7 min read · ↑ top

Codex Sites and open models

Hey folks,

I’m making progress on my agents manual! I think I finally figured out how I want the thing to look and feel.

I’ve built and rebuilt this damn thing so many times in this process, which is actually part of the process. I am a lazy workaholic (h/t Rick Rubin) - I have to spend time in the work, even if it feels like it’s not going anywhere, until ‘suddenly’ things click.

Whilst in the process, you find yourself wanting tools to exist to make things easier for yourself—that’s a huge part of why learning agents and how to steer them is so good.

You can build tools to enable you to build things.

I spun up this tool before bed last night where I can comment/delete on copy whilst I’m building, which I copy as one big block as agent feedback.

Ben Tossell

@bentossell

spun up a little text-editing tool with codex before bed like agentation but just for copy (supports keyboard shortcuts too ofc)

Attio is the CRM for the new way of GTM. Get agents working on every account, surfacing opportunities, and handle the work that used to take your team days. Open your inbox, the follow-ups are drafted. Walk into a meeting, you're already briefed. Got a question, just Ask Attio. Start for free today.

Headlines

Codex has two new additions: Plugins and Sites. Plugins are pre-built collections of skills, connectors to relevant apps (like Figma for designers) and instructions tuned for specific roles like data analysis and product design. Sites lets users create a shareable website/app with a database, file storage, env vars, access controls, and more. Initially only available to business and enterprise users.

A bunch of new open models released recently -

Gemma 4 12B - Multimodal (i.e. accepts images and audio as input) and performs nearly as well as the two-month-old 26B variant.

Ideogram 4.0 - 9.3B model for image generation. Trained on JSON prompts for control over the layout, colours and text for each element on the image. Also check Reve 2.0 for the focus on layout of elements in an image (but it’s closed-source).

Miso One - 8B text-to-speech model claiming expressive speech with 110ms latency.

Also, just like Cursor’s Composer, more companies are trying out fine-tuning big open-weights models for their domain-specific work. Latest entry → Harvey got a Kimi 2.6 agent to beat Opus 4.7 on its legal benchmark at ~11x lower cost.

Microsoft Scout is an always-on Microsoft 365 agent built on OpenClaw (reminder: openclaw is open-source). Different approach from what Google is doing with Gemini Spark.

Ramp Stack - An accounting assistant that helps with month-end close work: reconciling accounts, preparing schedules/accruals and more with reviewable sources. They also published a nice blog post explaining their efforts to benchmark Stack against other frontier models.

Financial fraud is evolving fast. It’s time to fight back—with AI. Read MIT Technology Review and Plaid’s report to see how technology is reshaping financial defenses. Learn more and see how smarter tools and industry collaboration can help fight against the rise of fraud. Read the report.*

My feed

Smallest AI lets you deploy voice agents at scale, powered by realtime STT & TTS and production-ready telephony infrastructure.*

Bloom turns your brand assets, site, decks, Figma and socials into a callable system that agents can use via API/MCP to generate on-brand assets.

Windsurf is now Devin Desktop. It manages fleets of local and cloud agents from the editor. Nous also released a desktop app for its CLI agent Hermes.

Hallmark v1.1 - open-source design skill for coding agents.

ViBench - benchmark from Replit with tasks focused on end-to-end app creation; Opus 4.8 beats GPT-5.5 on price/performance for vibe coding.

Skills for macOS - app for browsing and editing local skills, MCP configs and plugins.

Ollie - AI assistant for parents to manage the chores to free up time for family.

Television - visual workspace for personal agents. Notion-like kanban board vibes but with each tile attached to an agent.

Building software is learning - it’s an iterative process that will run into questions and obstacles. You should want that to happen as fast as possible.

Modern Engineering Values - a workflow and engineering values built after shipping several mostly or fully AI-written projects.

SDKs I’ve come across:

Email SDK - unified API for sending emails. works across multiple providers.

storagesdk - object storage with snapshots and forks.

Afters

Ethan Mollick

@emollick

Had Claude Code build a snake game where the snake becomes aware it is in the game and then... stuff happens. Some impressive creative decisions by the AI (& also some very AI ones), I just gave a first prompt and some feedback on the game as it went. snake-awakening.netlify.app

jules

@julesrosenberg

5 things @rauchg does differently > counts every keystroke he types per day > built a tool that lets him retroactively screen-record bugs > gives feedback in v0 instead of writing it out > gets a full company brain dump from an agent every Monday > doesn't keep a to do list

Paul Graham

@paulg

The most important component of writing clearly is simply to have high standards for clarity. Then if you write something unclear, you notice, and ask: what did I mean to say? You can just keep doing this over and over. And if you have high standards for clarity, you will.

Guillermo Rauch

@rauchg

YES-CODE An entire category of software, "no-code", was built under the presumption that code is expensive, difficult, and scarce. Coding agents have forever changed the equation. Code is now cheap, easy, and abundant. I remember @cramforce being asked by an analyst long ago:

Warp @warpdotdev

Our warp[dot]dev site gets 10M visitors/year. We migrated the whole thing from a no-code editor back to code in just 3 weeks. Very few hiccups, and SEO actually improved. Plus, the marketing team is free to use Warp to ship future changes

AA

@measure_plan

i made fruit ninja but you've got a guitar instead of a sword

AA @measure_plan

i made snake but the only way to move is by playing guitar chords

0xSero

@0xSero

I had a conversation Mario about electrical engineering, Pi, and parenting. Very grateful to get another chance to chat with one of my favorite builders and people. Enjoy (:

Peter Steinberger 🦞

@steipete

Here’s the video of my talk at MS Build: Build the thing that builds the thing.

| | build.microsoft.com

by Marcus Moretti Figma/ TL;DR:Spiralv4 just shipped with four major updates: a style engine that generates writing indistinguishable from your own 87 percent of the time, agent-native access via MCP, CLI, and API, team workspaces for writing in a shared voice, and a $10 price drop, bringing personal plans to start at $15 a month. Spiral will continue to be free for paid Every subscribers along with access to all our tools and content.Try Spiral 4.0

Today we’re announcing a number of updates to Spiral, the writing partner for you and your agent. Spiral is built by writers for writers, to help you from idea to line edit, matching your writing style throughout.

The highlights:

With stylometry (or the study of writing styles), Spiral now sounds more like you. We’ve built a new Style Engine from the ground up, so Spiral computes your writing fingerprint and picks relevant samples for new drafts.

Use Spiral wherever you do work. With a new MCP, plus our existing CLI and API, Spiral can step in if you’re underwhelmed by your agent’s writing output, or need good writing in any workflow.

For teams, use Spiral to speak with one voice. Team workspaces let you share styles, prompts, knowledge, and now chats and drafts.

And finally, we’ve given Spiral a new coat of paint and logo, designed by Daniel Rodrigues. The primary brand font is now Edgar, from Frere-Jones Type.

Since re-launching at the end of last year, Spiral has:

Created 5,524 from 168,464 writing samples

Generated 113,165 drafts

Made 350,078 revisions

It also now averages a 4.9/5 conversation score on our internal LLM-as-judge eval. We built Spiral to help people who write for work write better. Just as Cursor is a coding harness, Spiral is a writing harness, supporting you at every stage of the writing process. Here’s how:

When it’s time to draft , Spiral uses stylometry to reproduce your voice, working in Every’s know-how where appropriate. For example, if you ask Spiral for tweets, it will incorporate best practices from X’s latest algorithm update.

When you need help polishing a draft, Spiral is your editor. Along with a built-in guardrails against AI-speak, you can set custom writing rules that Spiral applies in a “top edit,” the final expert-level edit on a piece—a term I learned working at Every.

We’ve written about the challenges of getting LLMs to write like you. It’s difficult to prompt an LLM to write like you, let alone get it to stop using common AI phrasing and punctuation. Spiral’s Style Engine is the best solution to this problem we’re aware of. An eval runs on every draft Spiral produces, challenging an LLM-as-judge to spot the generated draft among real samples in a blind lineup. Today we’re at 87 percent on this eval, meaning Spiral’s generated draft blends in with users’ samples almost nine times out of 10. When a draft is spotted, the judge explains why, creating a feedback loop to refine the Style Engine further. Try Spiral 4.0

Spiral goes agent-native

As Dan Shipper has pointed out , Claude and Codex are increasingly becoming the central interface for all computer work. So we’ve made Spiral available to agents via MCP, CLI, and API. To try it out, copy and paste this command in your agent:

Help me set up Spiral, my AI writing tool, so you can write in my voice. Read https://writewithspiral.com/agents.md and follow the steps. In short: add Spiral’s remote MCP server at https://api.writewithspiral.com/mcp/ (Streamable HTTP). The first connection opens a browser to sign in to Spiral and authorize access (OAuth, no API key to paste). Then help me write something.

The CLI, or command-line interface, is personally how I use Spiral the most. After I merge a pull request, a cleanup command runs in Claude Code, which calls Spiral to generate tweets about the new feature for the Spiral X account. Spiral markets itself. This technique is now bundled into the compound engineering plugin in the form of the ce-promote command. In addition to the main spiral write command, the CLI and MCP, or model context protocol, expose “personalize” and “humanize” functions. “Personalize” takes a given piece of text and rewrites it in your voice. “Humanize” does a pass to remove common AI tells, including the dreaded em-dash (which Every’s house style uses, hence its appearance in this piece). Over 500 agents have been connected to Spiral since we launched the integration last month. Those agents are revising blog posts, generating marketing copy, drafting email replies, and more—automatically, and in the user’s voice. On some days, API sessions outnumber web sessions. And as agent-native usage of Spiral picked up, we realized we needed to adjust our pricing model. As a result, we’re adopting a new token-based pricing model, which is more in line with AI apps like Claude, Codex, and Cursor.

From session limits to token limits

In May alone, Spiral generated billions of LLM tokens, or units of text. While drafts typically range from 500 to 1,000 words, a lot of tokens are processed under the hood to make those drafts great. I’m reminded of the line attributed to French mathematician Blaise Pascal : “If I had more time, I would have written a shorter letter.” It takes a lot of tokens to generate a few good ones. Before this release, Spiral limited the number of sessions, or unique chats, users could start per month. This approach had two problems. First, some users sent hundreds of messages within a single chat, consuming tens of millions of tokens, while using only 2 percent of their session allotment. Second, API users hit their session limit quickly, because the shape of API usage tends to be many single-turn sessions. We’re moving to a token-based model, which is in line with how billing works in AI products like Claude and Codex. The personal and team plans come with millions of tokens each month. Once those tokens are consumed, it’s pay-as-you-go for extra token usage. Customers can disable extra usage and set their spend cap. The good news is that the base prices of the personal and team plans are both dropping by $10. Personal plans now start at $15 per month (down from $25), and team plans start at $25 per user per month (down from $35).

Tell your stories, express your ideas

Technology is at its best when it augments our skill sets—amplifying what we’re good at, assisting with what we’re not. Figma and Canva help designers do better work, and allow people without a design background to manifest what they imagine. Claude Code and Codex help engineers ship more software, and allow people without engineering backgrounds to create the software they always wanted to exist. Our hope is that Spiral helps writers sharpen their work, and allows people without a strong writing background to put their stories and ideas into words. One Spiral user is a retired musician in Australia. He’s accumulated a lifetime of stories in the studio and on tour. He’d never written them down, because he didn’t quite know how to tell them. Since signing up for Spiral, he’s recorded many chapters of his life stories with the tool’s help. He told me that Spiral has taught him how to be a better storyteller. That’s what we’re building toward: a writing partner that helps people say what they mean and get better at saying it. Spiral produces good writing fast, but it also explains its writing and editing decisions along the way: the rationale behind rhythm, structure, rhetoric, and more. As my colleague Natalia Quintero observed, the best AI tools teach you things as you use them. If any of this sounds useful, try Spiral. Share your feedback on X (@tryspiral) or get in touch: hi@writewithspiral.com. Try Spiral 4.0Marcus Morettiis the general manager of Spiral (@tryspiral).To read more essays like this, subscribe to Every , and follow us on X at @every and on LinkedIn.Subscribe

We’re launching a new section highlighting founders actively raising capital.

Every week I get flooded with messages from founders we’ve featured (and plenty we haven’t yet) wanting to share what they’re building, how fast they’re growing, what their revenue looks like, and who they’re raising from.

Some of those conversations are too interesting to keep behind closed doors.

With the founders’ permission, we’ll occasionally feature startups that are actively fundraising and give you a peek behind the curtain on what they’re building, where they’re at, and what their raise looks like.

Think of it as a curated founder-to-investor matchmaking section built right into the newsletter.

Back to the good stuff…

In this issue of the Stealth Startup Spy, here is what we will uncover:

MIT and Stanford-trained founder behind Topolabs (acquired by Autodesk) is building semi-autonomous robotics for wildfire prevention and precision forestry

Serial founder with exits to Intel, Check Point, and Proofpoint enters stealth

Former SVP at Cambr (acq. by NYSE: NBHC) is building an AI-powered treasury platform for local governments

Former Chief Strategy Officer at Boston Dynamics launches stealth robotics startup

Harvard MBA and former Uber Freight GM is building an AI-native logistics OS for healthcare and life sciences

And more…

Now let’s shine the spotlight… 💡💡💡

💰 Featured Founders Fundraising

Discover startups currently fundraising before they hit everyone’s radar.

FounderDNA: Serial Founder, Technical Founder, Doctorate Degree, Masters Degree, Top 10 University

Prior Experience: Ex-Senior Program Manager for Power and Propulsion, Lunar Fission Surface Power and Directed Energy at Lockheed Martin; ongoing Industry Advisor to NASA, US Space Force, and the Pentagon

Vaxon Space is developing satellite constellations in VLEO focused on missile defense and space-based interceptors, as well as AI / data center connectivity and enhanced ISR. They are a dual-use company supporting the DoW and commercial customers.

HQ: San Jose, California, United States

Traction and Highlights: Vaxon is currently fundraising through June 15 and filed provisional patents on inlet and pumping system with testing beginning in June. Anticipating approximately $3M in government funding wins across DARPA, NASA, AFRL and USSF.

🕵️♂️ Founders Coming Out of Stealth

Real-time updates from founders who debut what they’ve been working on under stealth mode

Prior Experience: Multiple GM Roles at Uber Freight, MBA at Harvard Business School, MS at UC Berkeley, Investment Manager at Verdane, Investment Manager at Equinor Ventures, Advisor at Porterbuddy

ZoomLogi is an AI-native logistics operating system for healthcare and life sciences, unifying carrier data, sensor feeds, and workflows to predict and automate exception resolution for pharmaceutical manufacturers, specialty pharmacies, biotechs, and logistics service providers.

FounderDNA: Serial Founder, Masters Degree, Former FAANG, Top 10 University

Prior Experience: Master of Public Policy at University of Chicago, Management Intern at Amazon, Associate Consultant at Altair Advisers, Commercial Strategy Intern at Gilead Sciences, Congressional Intern at U.S. House of Representatives

Nolro is an AI control plane that enables enterprises to approve releases, enforce guardrails, monitor drift and hallucinations, and generate audit-ready compliance evidence across AI systems, vendors, and workflows.

HQ: Chicago, Illinois, United States

Industry: AI Governance, Enterprise SaaS, Compliance Tech

FounderDNA: Serial Founder, Technical Founder, Masters Degree, Former FAANG, Top 10 University

Prior Experience: Engineering Manager at Amazon, Tech Fellow at Microsoft, Stanford University GSB (Corporate Innovation & Leadership), Founder & CEO at Voicy.AI, Founder at Jobsmunk

FounderDNA: Serial Founder, Technical Founder, Masters Degree, Prior Exit, Top 10 University

Prior Experience: Founder & CEO at Topolabs (Acquired by Autodesk), VP Software & AI at Stratasys, Founder & CTO at Riven, Senior Engineer at Intuitive Surgical, MIT and Stanford alum

Prior Experience: SVP, Head of Product and Operations at Cambr (acquired by National Bank Holdings Corporation, NYSE: NBHC), Strategic Initiatives and Operations at Keystone Industries

Edwin is the AI-powered treasury and financial platform built for local governments.

HQ: Santa Monica, California, United States

Industry: GovTech, FinTech, B2B SaaS | Team Size: 2

Time Spent in Stealth Mode: 6 months

🕵️♂️ Key Talent Going Under Stealth

Illuminating clues left behind by world class talent and influential innovators who just went into stealth mode

Neeraj Pradhan - Founder at Stealth Startup

FounderDNA: Technical Founder, Masters Degree, Former FAANG, Top 10 University

Prior Experience: Founding AI Engineer at LlamaIndex, Machine Learning Engineer at Meta, Research Engineer at Uber, Tech Lead AI Applications at Tribe AI

Etay Bogner - Co-Founder & CEO at Stealth AI Startup

FounderDNA: Serial Founder, Technical Founder, Former FAANG, Prior Exit

Prior Experience: VP and GM Zero Trust Products at Proofpoint, Founder & CEO at Meta Networks (Acquired by Proofpoint), Founder & CTO at Neocleus (Acquired by Intel), Founder & CTO at Stratoscale, Founder & Managing Director at SofaWare (Acquired by Check Point)

Prior Experience: Chief Product Officer at Self Financial, SVP/GM Commerce at HubSpot, Vice President of Product at Coinbase, Head of Product at Venmo, Staff Software Engineer at PayPal

Marc Theermann - Founder & CEO at Stealth Robotics Company

FounderDNA: Masters Degree, Former FAANG

Prior Experience: Chief Strategy Officer at Boston Dynamics, Director Global Partnerships at Google, EVP Strategy at Millennial Media (Sold to AOL/Verizon), Head of Mobile Platform Sales at Google

Prior Experience: Head of Engineering - CDP at Coinbase, Head of Engineering at ZORA, Staff ML Platform Engineer at Clubhouse, Member of Technical Steering Committee at x402 Foundation

🚨Here’s the deal 🚨This email has gotten too big. Exciting, but with more people following it, the edge diminishes. I’ve thought long and hard about what to do to preserve the value in the signals. I’m not sure about the final direction yet, but in the meantime I’ve been sending an email 48 hours earlier to a select group of paid subscribers. The feedback has been pretty positive so I’m going to open up the list for another 100 spots. To get signals early, Apply here!

Stay Stealthy,

Drake

Thank you for reading. If you liked it, share it with your friends, colleagues and everyone interested in staying ahead of the hidden developments in tech. Subscribe below and follow us onX / Twitter to never miss a company operating under stealth again.

Stealth Startup Spy is a data-driven newsletter for investors, journalists and tech enthusiasts interested in uncovering the next big move for key talent, real-time stealth company launches and technology advancements not in plain sight. We leverage the technology built at Gravity to shine a light on the hidden world of stealth startups.

Spiral 4.0 introduces a new style engine, why enterprise roadmaps are hard, and a workflow for making your coding agent more efficient

by Laura Entis ### Launch

Spiral 4.0

Today we’re launchingSpiral4.0, which writes drafts in your voice from idea to line edit. Spiral has a new MCP alongside the existing CLI and API, so any agent or workflow can write in your voice too. For teams, we’ve expanded workspaces, which let you share styles, prompts, knowledge—and now chats and drafts. Finally, Spiral has a new pricing model: We’ve switched from session limits to token limits, so costs match your actual usage rather than how many times you opened a new chat. A vast majority of users will end up paying less: Personal plans now start at $15 a month—down from $25—and team plans are $25 per user, down from $35. Try Spiral 4.0

Signal

Enterprise AI product roadmaps are hard

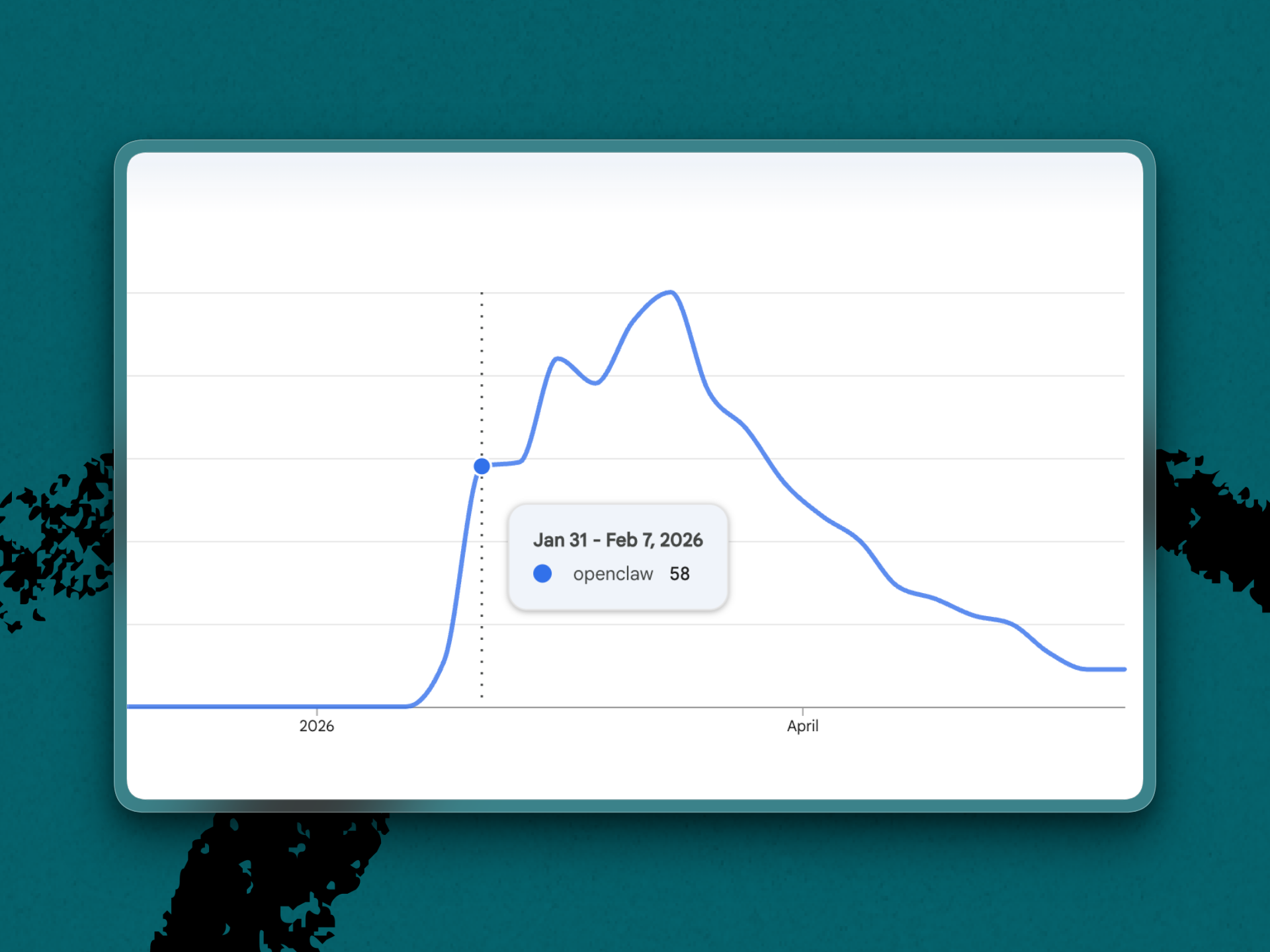

Microsoft is moving fast. Three months after OpenClaw came out in November 2025, Microsoft CEO Satya Nadella described it as a “virus”-like security risk. By May, the company’s “Project Lobster” was internally testing “ClawPilot,” an OpenClaw-based desktop environment. This week at the Microsoft Build conference, the company released Scout , a personal agent for work built on OpenClaw. For a company employing 100,000 engineers, this is blindingly fast. Unfortunately, it may already be too late. The Google Trends graph for the term “openclaw” shows search interest spiked in January and began its descent soon after. (Screenshot courtesy of Mike Taylor.) OpenClaw search traffic spiked in early January, after everyone had a chance to experiment with Opus 4.5 over the holidays. The sharp rise in interest died down almost as quickly as it took off, helped along in early April by Anthropic ending support for subsidized Max plan usage —thereby forcing everyone to scramble to get OpenClaw working on cheaper models. This doesn’t mean OpenClaw is dead; the open-source project saw a recent uptick in download and is still under active development, with millions of dollars of patronage from OpenAI, which hired its creator Peter Steinberger. AI agents as a category aren’t dead, either, as traffic has moved to other agents like Hermes, Google has just rolled out Gemini Spark (first announced last month at its I/O developer conference), and Claude and Codex have both adopted more agentic features inspired by OpenClaw. That said, it must be tough to manage enterprise AI product roadmaps these days. You do everything right, watch the latest trends, pivot your focus to supporting new tools and making them secure in enterprise environments. You move mountains to explain to stakeholders why this is a good idea. You plan the keynote of your big conference, which has to be scheduled months in advance. Then a month after the internal beta (just three months since the tool went viral), you’re already behind the news cycle. Everyone has moved onto the next shiny thing. You go back to the drawing board and think “maybe next time, we’ll just announce it on X.”— Mike Taylor

Log on

Get hands-on with how Every uses AI. These are the live camps, workshops, and meetups where team members teach the workflows behind our work.

These days, Monologue ’s general manager Naveen Naidu spends most of his time in the Codex app with Fin—formerly Intercom, a customer support platform—open in the coding agent’s in-app browser. Working from a repository-local project, he has Codex investigate the customer issue displayed in the browser, create a bug report in Linear, link the Intercom ticket to the Linear issue, and draft a reply to the customer with information about the bug report—all without having to leave the app. Fin has an MCP with 13 common actions, like searching conversations or reading and writing messages. Naveen’s workflow required a more specific one: Turn the active Fin conversation into a markdown file the coding agent could read. Here’s Naveen’s workflow for creating a more focused setup ...

You're among 70,562 others who received this email because you wanted a weekly recap of the best articles from Hacker News. Published by Curpress from Bellingham, Washington. Hacker Newsletter is not affiliated with Y Combinator in any way.

✨ Want to promote your startup? Buy a classified ad or click reply to get our media kit

Every week I’ll provide updates on the latest trends in cloud software companies. Follow along to stay up to date!

Where Are the American Open Source Models?

I’ve been investing in open source companies for nearly my entire venture career. I love open source businesses, think they’re generally great for the ecosystem, and can also create a lot of commercial value (but this can be tricky!). We’ve seen all kinds of open source businesses become successful. Databases (Mongo, Clickhouse, etc), Data Infrastructure (Databricks, Confluent, etc) Developer Tools (Hashicorp, GitLab, etc). And many other categories.